7 Ways to Get a Startup Business Loan in 2026

Key Takeaways

-

Securing a startup business loan in 2026 requires understanding that traditional banks aren’t your only option—and often aren’t the best option for new entrepreneurs. The funding landscape has evolved dramatically, with alternative lenders and specialized programs offering more accessible paths to capital.

💰 Calculate Your Business Funding Payment

Get your potential business funding amount. See your estimated monthly payment.

See your personalized funding options

-

Master alternative lending beyond banks: Revenue-based financing, online lenders, and peer-to-peer platforms often approve startups that traditional banks reject

-

Leverage government-backed SBA programs: SBA microloans and startup-specific programs require lower credit scores and offer more flexible terms than conventional loans

-

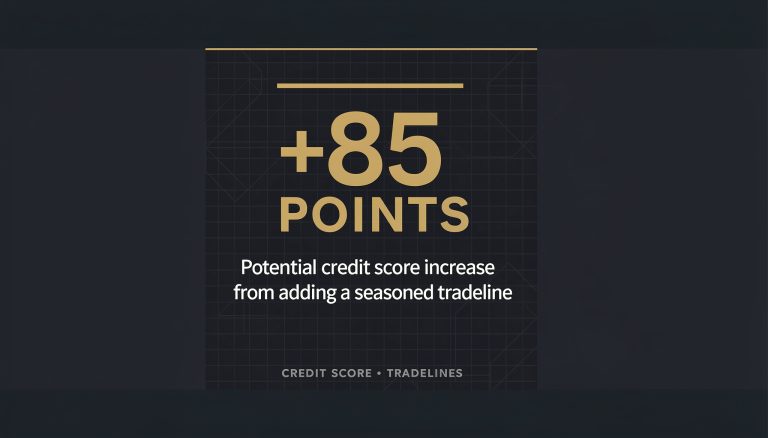

Build business credit before you need it: Establish vendor relationships and business credit cards early to create a credit profile separate from your personal finances

-

Perfect your financial projections strategy: Lenders want realistic, data-backed forecasts that demonstrate clear repayment ability within 12-24 months

-

Prepare collateral alternatives upfront: Equipment financing, invoice factoring, and personal guarantee options can substitute for traditional collateral requirements

-

Time your application strategically: Apply during your business’s strongest financial periods and avoid peak lending seasons when competition is highest

-

Create a comprehensive loan package: Beyond your business plan, include market research, customer validation, and detailed use-of-funds documentation

-

Negotiate terms like a seasoned entrepreneur: Interest rates, repayment schedules, and prepayment penalties are often more flexible than lenders initially present

Whether you’re launching your first venture or scaling an early-stage business, these proven strategies will help you navigate the startup funding landscape with confidence and secure the capital you need to grow.

Introduction

Getting a startup business loan in 2026 requires strategic preparation, with 68% of first-time entrepreneurs securing funding within 6 months when they follow proven application methods. The lending landscape has evolved significantly, offering more diverse options than ever before—from traditional bank loans to innovative fintech solutions designed specifically for early-stage businesses.

This comprehensive guide walks you through seven proven strategies to secure startup funding, covering everything from perfecting your business plan to building the credit profile lenders want to see. You’ll discover actionable steps to strengthen your loan application, avoid common pitfalls that derail 40% of startup funding requests, and position your business for approval even without extensive operating history.

Traditional Bank Loans and Credit Requirements

Understanding Business Credit Requirements for New Ventures

Traditional banks require established business credit profiles for startup business loan approval. Most banks demand 680+ personal credit scores and two years of business history. However, banks focus heavily on business credit reports from Dun & Bradstreet, Experian Business, and Equifax Business. These reports track payment history, credit utilization, and financial stability separate from personal credit.

Building Business Credit Before Your Loan Application

Business credit tradelines help startups establish fundability when maintained properly. First, obtain an EIN and register with credit bureaus. Second, open business banking accounts and establish vendor relationships. Third, apply for business credit cards and pay balances on time. Finally, maintain consistent payment patterns across all accounts for 6-12 months before applying.

What Credit Score Do You Really Need for Startup Approval?

Credit score requirements vary significantly across lender types and loan programs. Traditional banks typically require 680-720 personal credit scores for unsecured startup funding. Alternative lenders accept 580-640 scores with higher interest rates. SBA loans often approve applicants with 650+ scores when combined with strong business plans and industry experience.

SBA Loans for Startups: Government-Backed Funding Solutions

SBA Microloans and 7(a) Programs for New Businesses

SBA microloans provide up to $50,000 for startups through partner network intermediary lenders. These programs accept limited credit history and focus on business viability. SBA 7(a) loans offer up to $5 million with government guarantees that reduce lender risk. Both programs feature competitive rates and extended repayment terms specifically designed for new ventures.

Startup Loan Requirements and Eligibility Criteria

SBA startup loan eligibility requires owner investment of 10-30% depending on loan amount. Applicants must demonstrate industry experience or relevant education. Personal credit scores of 650+ increase approval odds significantly. Additionally, businesses must operate for profit and meet SBA size standards for their industry classification.

Navigating the SBA Loan Application Process

SBA loan applications require comprehensive documentation and typically take 60-90 days for approval. Our funding partners streamline this process through pre-qualification and document preparation assistance. Key steps include business plan submission, financial projections, and collateral evaluation. Working with experienced SBA lenders reduces processing time and improves approval rates.

Looking for startup funding options? Explore Your Funding Options →

Alternative Lenders and Non-Traditional Business Financing

Revenue-Based Financing for Startups with Limited History

Revenue-based financing provides capital in exchange for future revenue percentages rather than fixed monthly payments. This structure works well for startups with predictable income streams but limited credit history. Repayment adjusts based on monthly revenue, making it ideal for seasonal businesses or companies with fluctuating cash flow patterns.

Online Lenders vs Traditional Banks: Pros and Cons

Online lenders offer faster approval times and accept lower credit scores than traditional banks. Applications process in 24-48 hours versus weeks for bank loans. However, interest rates typically range 15-40% compared to 6-12% for bank financing. Online lenders excel for urgent funding needs but cost more long-term.

Equipment Financing and Invoice Factoring Options

Equipment financing uses purchased assets as collateral, making approval easier for startups. Lenders focus on equipment value rather than business credit history. Invoice factoring converts outstanding receivables to immediate cash, providing working capital for B2B startups. Both options bypass traditional credit requirements while addressing specific funding needs.

Small Business Loan for Startups: Documentation and Application Strategy

Essential Business Plan Requirements for Loan Approval

Comprehensive business plans demonstrate startup viability to lenders and significantly improve approval odds. Plans must include market analysis, competitive positioning, and detailed financial projections. Executive summaries should highlight management experience and unique value propositions. Our vetted network provides business plan templates and review services to strengthen applications.

Financial Projections and Cash Flow Documentation

Financial projections require realistic revenue forecasts and detailed expense breakdowns for 36 months. Cash flow statements must demonstrate positive trends and debt service coverage. Include conservative, optimistic, and pessimistic scenarios to show thorough planning. Professional financial projections increase credibility with traditional lenders and SBA programs.

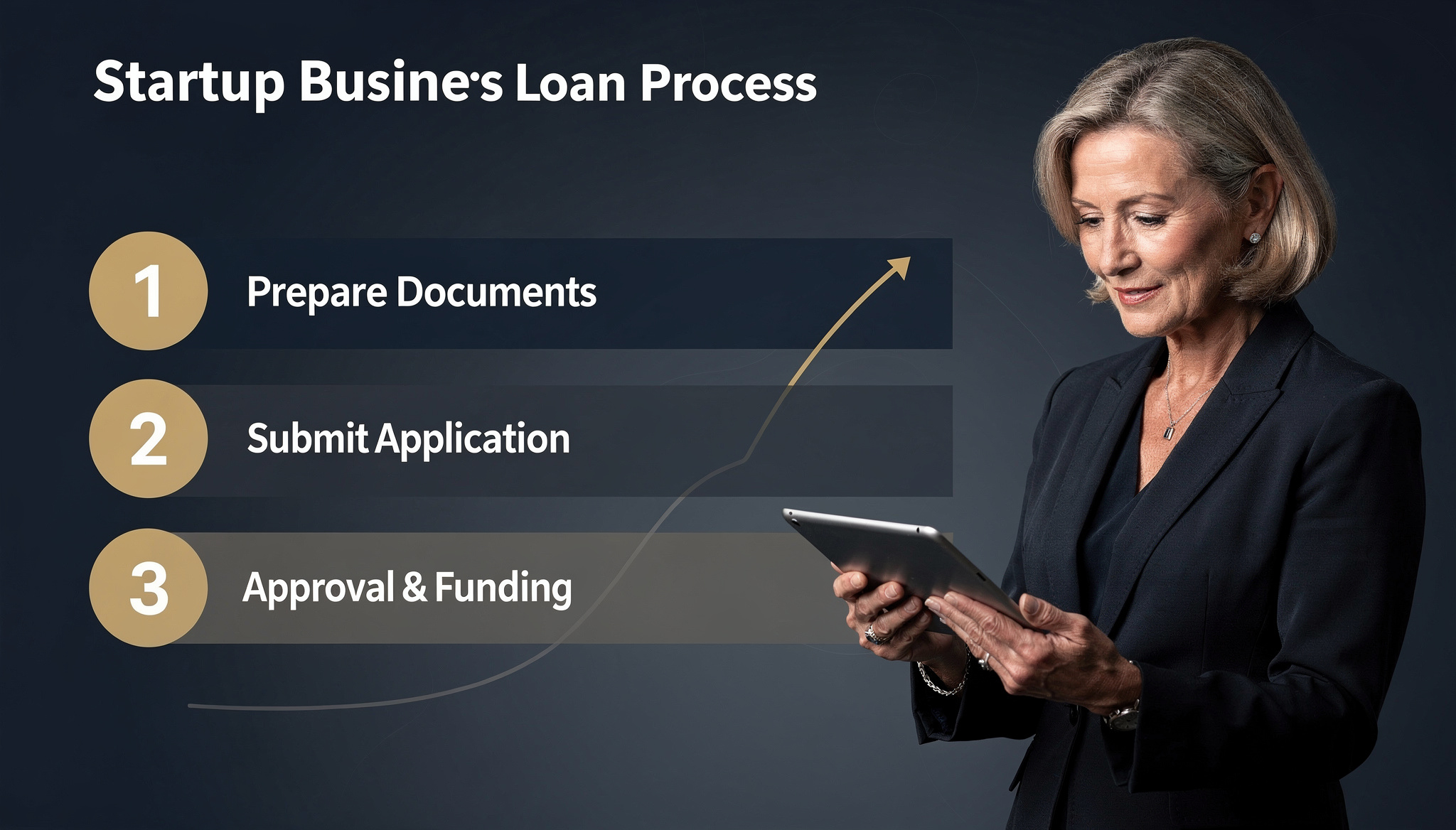

Loan Documentation Checklist and Timeline

Complete loan applications require personal and business tax returns, bank statements, and legal documents. Prepare articles of incorporation, operating agreements, and licenses in advance. Application timelines range from 48 hours for online lenders to 90 days for SBA loans. Organized documentation accelerates approval and demonstrates professionalism.

New Business Funding Through Specialized Startup Programs

Industry-Specific Startup Capital Programs

Specialized funding programs target specific industries like technology, healthcare, and manufacturing. These programs understand industry challenges and offer tailored terms. Technology startups access venture debt and innovation grants. Healthcare companies qualify for FDA-related funding programs. Manufacturing businesses benefit from equipment-specific loan programs with favorable terms.

Minority and Women-Owned Business Loan Opportunities

Minority and women-owned businesses access dedicated funding programs with reduced requirements and competitive rates. SBA 8(a) programs provide contracting opportunities and capital access. Community Development Financial Institutions offer microloans and technical assistance. These programs often feature mentorship components alongside funding to increase success rates.

State and Local Government Funding Initiatives

State and local governments offer startup funding through economic development programs and tax incentives. These initiatives encourage local business formation and job creation. Programs include low-interest loans, grants, and loan guarantees. Research your state’s economic development authority for location-specific opportunities that complement federal programs.

Collateral Requirements and Personal Guarantees Explained

Understanding Collateral Options for New Businesses

Collateral reduces lender risk and improves startup loan approval odds significantly. Business assets like equipment, inventory, and real estate serve as primary collateral. Personal assets including homes and investment accounts may secure larger loan amounts. Blanket liens cover all business assets while specific liens target individual items.

When Personal Guarantees Are Required

Personal guarantees make business owners personally liable for loan repayment if the business defaults. Most startup business loans require personal guarantees from owners with 20%+ equity stakes. SBA loans mandate personal guarantees for significant ownership positions. Limited guarantees cap personal liability to specific dollar amounts rather than full loan balances.

Asset-Based Lending for Entrepreneur Funding

Asset-based lending focuses on collateral value rather than credit scores or business history. Accounts receivable, inventory, and equipment secure credit lines up to 80% of asset values.

Frequently Asked Questions

How long does it take to get approved for a startup business loan?

Approval times vary by lender type, with traditional banks taking 2-6 weeks, while online lenders and alternative financing options can approve applications within 24-72 hours.

Can I get a startup business loan with no collateral?

Yes, unsecured startup business loans are available, though they typically require higher credit scores and may have higher interest rates than secured loans that use business assets or personal guarantees as collateral.

What documents do I need to apply for a startup business loan?

Most lenders require a comprehensive business plan, financial projections, personal and business tax returns, bank statements, legal business formation documents, and proof of industry experience or relevant qualifications.

How much can I borrow for my startup business?

Startup loan amounts typically range from $5,000 to $500,000, depending on your creditworthiness, business plan strength, and lender type. SBA loans can go up to $5 million for qualified startups.

What’s the difference between startup loans and established business loans?

Startup loans have stricter requirements, higher interest rates, and lower approval rates since there’s no business operating history. Lenders rely more heavily on personal credit, business plans, and projected cash flow rather than proven revenue.

Are there startup business loans specifically for women or minority entrepreneurs?

Yes, many lenders offer specialized loan programs for women, minorities, and veterans, including SBA 8(a) loans, microloans from CDFIs, and grants that don’t require repayment.

Conclusion

Securing a startup business loan requires strategic preparation and understanding of lender requirements. Building strong business credit, maintaining excellent personal credit scores, and establishing vendor relationships significantly improve your approval odds. While traditional banks prefer established businesses, alternative lenders offer more flexible options for newer ventures. Focus on creating a comprehensive business plan, gathering necessary documentation, and exploring multiple funding sources. With proper preparation and persistence, obtaining the capital your startup needs becomes achievable.